In the past days two interesting articles around banks and banking innovation found their ways into my browser. One by Knowledge@Wharton on “How Banks Can Keep Up With Digital Disruptors” and the second one by Mobile Commerce Daily on “How four Australian banks are challenging Apple’s stranglehold on mobile payments”.

The first article is essentially stating that banks are not using the “essential assets need to turn aside many of the assaults on their business now underway from fintech”, while the second one seems to sing the song of the poor banks that are held at a disadvantage by evil Apple.

The four banks that challenge Apple are Bendigo and Adelaide Bank, Commonwealth Bank of Australia, National Australia Bank, and Westpac. Another large bank, ANZ Bank, cooperates with Apple by offering their customers to import cards into the Apple Wallet and using Apple Pay, and is not involved.

But what do the banks want? According to the article they want access to “Apple’s Apple Pay system as well as access to the NFC capabilities of the iPhone”, being narrowed down to “require Apple to only disclose access to the NFC capabilities of the iPhone to the banks and therefore their customers.”

Essentially they want to be able to build their own mobile payment system and not go through Apple’s wallet and still be present on “one of the most popular smartphones in the world”

And yes, it is true that Google’s Android operating system allows more access to the phone’s NFC capabilities than iOS.

On the other hand banks are seeing disruption coming. Fintech companies are coming up left, right, and center, attacking banks’ business models, offering payments, simple international transactions, advice, finance- and wealth management, lending services, even alternative currencies. The list goes on.

By the Numbers

Still, the question remains whether there is a ‘stranglehold’ that deprives the banks of their ability to compete. After all it seems possible to work with Apple, as evidenced by ANZ. Also, the market share of iPhones sales worldwide in Q4/2016 has been 18.3 percent (up from 12.4 percent in Q3/2016), according to Statista.

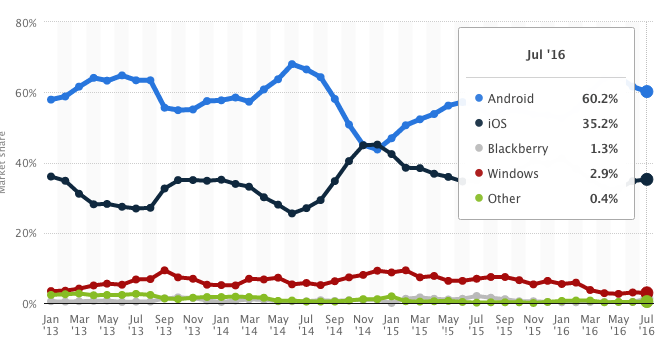

As it turns out the market share of iOS devices in Australia is at around 35 percent in July 2016, again according to Statista.

Australian Mobile OS Market Share

Source: Statista

Let’s assume that all of these are iPhones as the title suggests. In this case the banks to not have direct NFC access to about a third of all devices; in case this data covers both, iPhones and iPads, it is about half of this figure, which correlates to the worldwide sales data.

Older Business Insider data about revenue distribution by country and platform shows about an even distribution of sales on iPhones vs. Android devices. The same article also observes a socio-economic split between iPhone and Android users in the US, a split in favour of iPhone. Simply put iPhone users are more affluent, although they seem to spend less per order than Android users. The Q4/2016 Monetate Benchmark report confirms this by finding an approximately 20% higher order value on iOS devices than on Android devices.

My Take

“Banks seem to be headed the way of Blockbuster” is what the Wharton authors are saying. What in my experience also seems evident is that banks still need to transform from rigid organizations to businesses that are truly offering value to their customers. I have written about some personal experiences about bank shortcomings before, here, too.

Banks’ main problem is not that they are not having full access to iPhone functionalities, but that they haven’t yet understood how to regain the trust that they need to have, to stay relevant.

People more and more prefer to get banking services from a non-financial services company.

That is their problem!

Not that they cannot create an end-to-end payment system that they control – a market they are not in now.

Banks are asking where they can have or get an additional advantage. They are not asking the question where they can provide real value to their customers.

Being an occasional user of both, a banking app as well as Apple Pay (I am an ANZ customer) I ask myself where the bank’s access to the NFC chip offers value for me.

I don’t see any.

Why?

Apple’s wallet is tightly integrated into the phone. Double click the button on the lock screen and the payment system is up. How can the bank make this simpler for me? Siri? I doubt it – “Open Wallet” opens … Surprise … Apple’s wallet. Open ANZ doesn’t do the thing and “Open ANZ app” is already longer.

Do I really use the banking app?

No!

Why?

Because I rarely need it.

It doesn’t add much value. It is fairly cumbersome. At this time it even doesn’t allow me to log in using my fingerprint.

So, in summary the legal action that is pursued by the banks is not about creating value for (or with) their customers but about gaining entry into an additional revenue stream for themselves.

What can the Banks do?

In simple words: Become trustworthy partners of their customers again.

Banks have a tremendous amount of knowledge about their customers. This can be used for very personalized services.

With their branches they have assets with direct access to customers. Yet branches seem to come out of fashion with their executives, getting closed or at least are pretty dull. Can there be more experience?

Look at terms, conditions, and fees. There are reasons why people to transfers with non-banks: It is cheaper, faster, easier. Why do banks make it my problem if an international money transfer doesn’t reach its destination after paying for the service and getting a bad conversion rate?

There is reach. In the past century banks managed to move themselves in a position that makes them indispensible. This is not an entitlement, nor a given. Exhibit customer orientation, innovate around the customer – and with the customer, showing clear value for the customer, using an outside-in point of view as opposed to the current inside-out one.

It all starts from trust and value.