As it is the case for most of my colleagues I regularly get pitched by businesses about customer experience news that they want to talk about and that normally are pretty interesting. So, also a few days ago, when I got pitched by AR relations of a major European bank that wanted to talk about a new partnership and “what personalisation tech can offer in terms of a way to side-step legacy tech barriers to provide meaningful customer engagement that goes far beyond “Dear Joe” but that provides customers with what they need, when they need it”.

The backdrop of this story is, of course, the advent and rise of fintechs like Revolut, N26, or Monzo. These are the ones that got named in the pitch and that are representatives of many more fintech companies that are disrupting traditional banking. We could add some more like Weltsparen, Transferwise, and other services that target at disrupting one or the other part of banking.

And banking is surely an interesting sector of B2C as well as B2B business that is highly regulated, often very conservative, and burdened with legacy IT systems, to name but a few challenges facing banks.

All these topics are making them an interesting target for nimble companies that, amongst others, are engaging with their customers in a highly personalised manner. This is very much in line with the research report by Epsilon that got quoted in the pitch.

Consequently, personalisation is a very good start.

However, there is more.

The model of the quoted fintechs is not only to provide a high degree of personalisation. They are also striving to deliver services that the customers want, and the way they want it, at a price point and to conditions that serve the customers more than what they currently get.

The bottom line is that customers have lost trust in banks. They do not believe anymore that banks have their best interests in mind when offering a service.

Examples of these improved services that are manifold, most of which we know from own experiences.

- Look at account fees, or fees for withdrawing from or depositing moneys to your accounts. These are still far too common

- Ever tried to do an international money transfer? Not only are these usually slow, but also very expensive. On top of that banks regularly make you agree to a clause that any loss of the money is your problem, not theirs

- Investment advice is regularly favouring products that provide a high commission to the bank, while you are made to sign forms that basically remove the bank you are dealing with from any responsibility

- Changes in reference interests are regularly treated in two ways: If they go up, the rates customers have to pay go up almost immediately; if they go down, things move at a far more leisurely pace

- The GFC, that started as a mortgage crisis, and how many mortgage banks treated defaulting customers, is a story all of its own

This list can go on and on.

There is a seemingly never ending series of news about fraud and manipulation of markets, creativity in finding new fees, poor customer service at hotlines, clunky processes and you name it. Think of Deutsche Bank, Morgan Stanley, or Wells Fargo if you need any examples of scandal. Think about the so-called Panama files if you want to get a little further.

As a result, banks are perceived as not being innovative in providing services that customers regard as being valuable or that are right in the field of immoral or even illegal. All this in the name of profitability.

The consequence of this is a lack of trust.

Now, don’t get me wrong, not everything is hunky dory in fintech land, too, as you may have seen if you followed the news about the recent blunders of N26, who look at a superior customer experience as their unique selling proposition.

Personalisation, at its heart, is about providing customers with a messaging that is closely related to their individual interests, in real time, across channels. But as such, it first of all is a marketing tool.

So, personalisation is a good start, but it is just that, a start.

What is needed?

Everything boils down to delivering value to customers. Banks need to be perceived as trustworthy guardians of the moneys they are entrusted with. They need to be seen as the ones that have their customers’ interests at heart, and not their own profit.

The key to this is applying an outside-in view, thinking about and identifying what customers need and want in the various situations they find themselves in. Almost trivial examples of what customers want include

- Having money in accounts safe and secure

- Being able to easily open up an account

- Being able to transfer moneys fast, easily and reliably at competitive rates

- Getting a mortgage at competitive rates with no major fuss

- Receiving competitive interest rates on their savings accounts

- Receiving reliable and accurate service whenever needed

To be sure, there are many more.

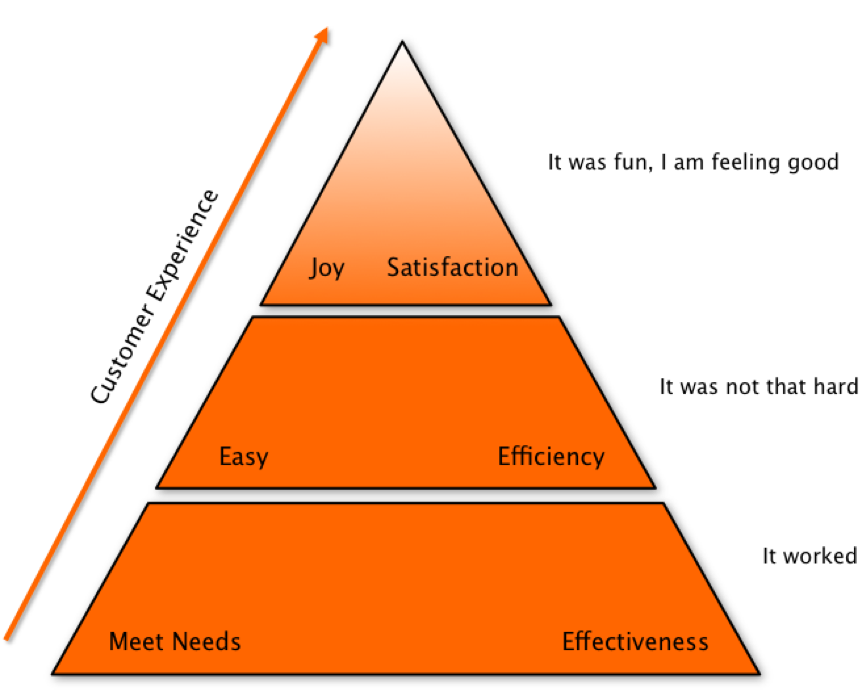

Customer Expectations Hierarchy

Customers are after an outcome when interacting with a business. They want or need to address a situation that requires a solution that creates value for them. Applying an outside-in view on these customer desired outcomes, with the intent of creating value for and with customers results in a mindset that identifies what is of value for customers and helps in creating this value for and with them. Simply put: Look at yourself with your customers’ eyes.

This mindset makes own profit the desired result, not the overarching objective.

And yes, banks are businesses, they are allowed and required to make profits.

Once the customer outcomes that a bank wants to deliver to, are identified, the next step is establishing how this can be achieved most efficiently for both parties. It is here that personalisation, even individualisation, comes into the equation. Additional important tools at this stage are customer journey mapping and the design of interaction points in a way that minimizes friction for the customers on the way of achieving their desired outcome and creating their value.

Lastly, treat customers as humans. Make them feel valued by valuing their most important asset, their time. Make interacting with yourself enjoyable for them.

That will create loyal customers that want to return.

Doing this goes well beyond personalization. It is a corporate endeavour that stretches the complete value chain, be it a bank’s value chain or any other type of business.

Businesses, especially banks, need to address customer experience to thrive, instead of looking at aspects like personalization. Doing the latter only strengthens the story of disruptive fintechs.