by twieberneit | Feb 15, 2017 | Blog |

In the past days two interesting articles around banks and banking innovation found their ways into my browser. One by Knowledge@Wharton on “How Banks Can Keep Up With Digital Disruptors” and the second one by Mobile Commerce Daily on “How four Australian banks are challenging Apple’s stranglehold on mobile payments”. The first article is essentially stating that banks are not using the “essential assets need to turn aside many of the assaults on their business now underway from fintech”, while the second one seems to sing the song of the poor banks that are held at a disadvantage by evil Apple. The four banks that challenge Apple are Bendigo and Adelaide Bank, Commonwealth Bank of Australia, National Australia Bank, and Westpac. Another large bank, ANZ Bank, cooperates with Apple by offering their customers to import cards into the Apple Wallet and using Apple Pay, and is not involved. But what do the banks want? According to the article they want access to “Apple’s Apple Pay system as well as access to the NFC capabilities of the iPhone”, being narrowed down to “require Apple to only disclose access to the NFC capabilities of the iPhone to the banks and therefore their customers.” Essentially they want to be able to build their own mobile payment system and not go through Apple’s wallet and still be present on “one of the most popular smartphones in the world” And yes, it is true that Google’s Android operating system allows more access to the phone’s NFC capabilities than iOS. On the other hand banks are seeing disruption coming. Fintech companies are coming up left,...

by twieberneit | Jul 11, 2016 | Blog |

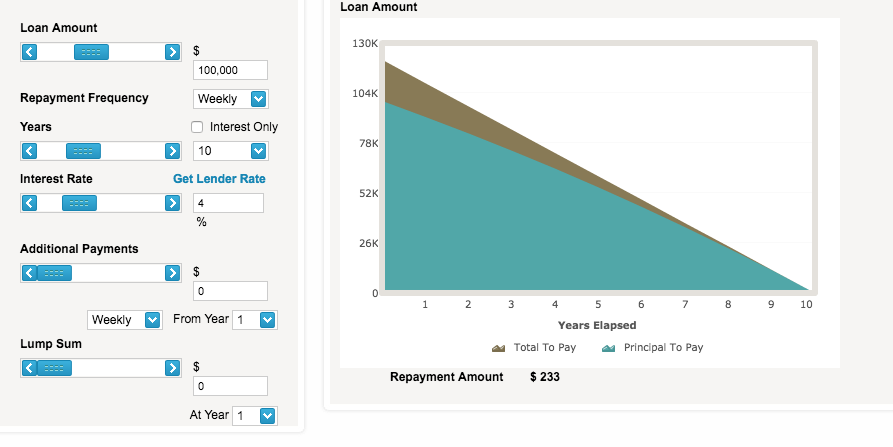

After some investigation into SME CRM Nimble and Freshsales and travel management software traform today is the day of a reflection on customer orientation in one of the industries that managed to become almost indispensable in our lives. Banks. So let me tell you A Bank Tale of Mystery and Imagination But not an invented one. This is life in 2016. Imagine the following extremely uncommon scenario: You want a mortgage for a house. Imagine also that you have a fairly good income, so you want to pay down fast. After all interest rates in NZ are still pretty high compared to other developed nations – although they are very low for NZ standards. And remember – one of the basic premises of neoliberalism is that everybody has equal negotiation powers (the Kiwi in me says “Yeah, right” to that one …). What are the variables you have in a mortgage? The total amount, interest rate, pay down period, term of fixing the interest rate, unless you go floating, that is, and the start of the pay down. So you start doing some maths on what you are able and willing to regularly pay and start negotiating a rate, finally coming to an agreement, clearly communicating that you want a fixed term of one year, and a calculated pay down period of, say 10 years, and weekly payments. You are happy. The documentation arrives, actually three pieces of it. A summary of the agreement Terms and Conditions on about 30 pages of legalese. No need to go through it here; it basically details out that the bank has all...